SUMMARY: Benchmark research from North American news media companies indicates acquisition of digital products is likely to remain at current levels without a significant news event occurring to increase traffic.

Satisfying Audiences Blog | July 26, 2022

By Matt Lindsay, President of Mather Economics

Mather Economics publishes quarterly benchmark reports for news media subscriptions and digital audiences. We’d like to share our perspective on the future of news subscriptions in light of recent trends in the benchmarks for subscription volumes, new customer acquisitions, and average rates.

The subscriber benchmarking data comes from more than 300 newspapers in North America. We receive this data weekly through our ongoing work with these publications. To be included in this report, Mather must have 13 months of weekly subscriber data from a publication.

Data on digital audiences is collected using the Listener Data Platform, a first-party tracking tool that captures browser click-stream data from anonymous and known users, events from mobile applications, advertising impressions, and paywalls. This data is standardized and consistent across participating publications, which makes this data set unparalleled in the media industry for breadth, frequency, and consistency.

Mather Economics also shares anonymized data on digital subscribers and engagement with the Medill Journalism School at Northwestern University through its Subscriber Engagement Index.

Subscription trends and benchmarks

New subscriber acquisition

- Acquisition volumes have returned to pre-pandemic levels for many publishers due to reduced digital audience traffic.

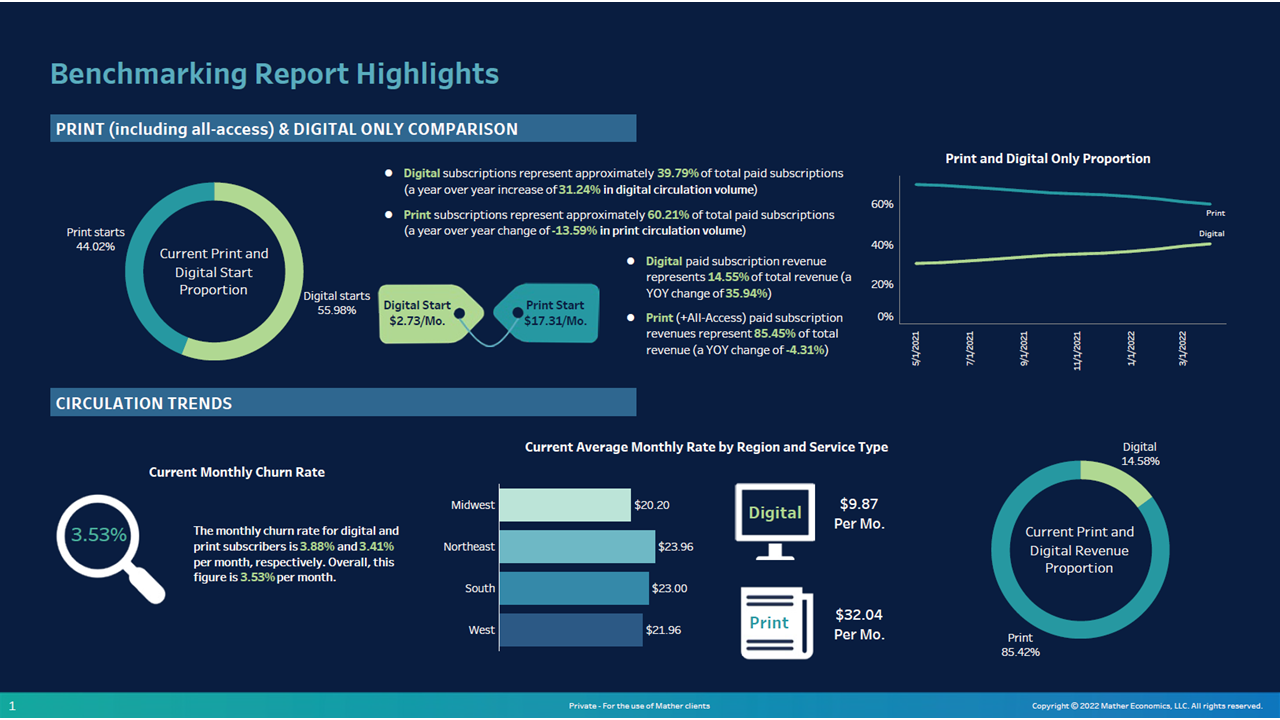

- Digital-only acquisitions exceed hybrid subscriptions. New subscription sales volumes are 56% digital-only and 44% hybrid.

- Digital-only subscription volumes have increased by 23%. Hybrid subscription volumes have decreased 19% on average year-over-year.

- The average acquisition price of new digital-only subscriptions is US$2.73 per month and US$17.31 for hybrid subscriptions.

- There is a trend toward longer-term, lower-priced promotional offers for digital-only products. Many publishers benefit from increased conversions and greater net lifetime value even with increased churn from subscribers moving from promotional to “regular” prices following the promotion.

Subscriber retention and engagement

- Retention for subscriptions has decreased in 2022 versus 2021 due to the elevated start levels last year.

- Monthly churn is 3.9% for digital subscribers and 3.5% for hybrid subscribers.

- Overall, subscription volume is down 9%.

- Many publishers have successfully mitigated churn by using engagement triggers (such as deviations from engagement patterns) to drive retention campaigns for at-risk subscribers.

Subscriber volume and revenue

- Digital-only products are 15% of subscription revenue and 40% of volume.

- Hybrid product revenue is 85% of total subscription revenue and 60% of volume.

- Standard prices for subscriptions are increasing for both digital and hybrid products.

- Average digital prices are still much lower than hybrid subscriptions even when controlling for the different average tenures of these customers.

- The average monthly price for digital-only products is US$9.87 versus an average price of US$32.04 for hybrid products.

2022 subscription predictions

Prediction #1: Impact of the news cycle on traffic patterns and subscriber growth

- Mather Economics forecasts acquisition of digital products will remain at current levels without a significant news event occurring to increase traffic.

- The war in Ukraine has not increased subscription starts for regional and local news organizations as it has for global news brands. Consumption of pandemic coverage has declined as audiences return to pre-COVID-19 consumption patterns.

- The election cycle in 2022 will increase traffic levels later this year, but mid-term elections in the United States do not match presidential election years for audience growth.

Prediction #2: Impact of global economic trends and costs

- A mild recession in the United States is likely already underway, but employment levels remain high relative to prior recessions. This is a cause for optimism that advertising revenue will not decline significantly and consumer spending on subscriptions will remain steady.

- Election spending on advertising will help with ad revenue through the end of the year.

- Challenges to delivery networks will continue due to high employment levels and elevated gasoline prices.

- Publishers are continuing to optimize their subscription delivery footprints and focus on operating margins from subscribers as they transition customers to digital-only products.

Prediction #3: Impact of new opportunities and revenue streams

- Opportunities for new revenue streams have increased due to the growth in sports betting, a return to in-person events, and e-commerce businesses.

- Business models for newspapers of different sizes are diverging with regard to their mix of revenue streams. Small-market newspapers have less potential digital subscription revenue and will continue to rely on advertising and other revenue streams. Global, national, and large regional titles have greater potential digital subscription revenue, and they are experimenting with new digital products and services.

For more information, connect with Matt at matt@mathereconomics.com.

Mather provides strategic insights to the newspaper industry through its quarterly benchmark reporting.

Click here to download your free report

Please contact Mather Economics if you would like to participate in our benchmarking reports or have any questions. Mather is developing benchmarks for other regions with more details to be announced later this year.