By: Madelin Zwingelberg, Consulting Director and Pete Doucette, Sr. Managing Director

For years, digital subscription growth was viewed primarily as an audience problem. The assumption was straightforward: grow the audience, and subscriptions and revenue would follow.

Audience still matters, but Mather’s Subscription Proficiency Index (SPI), which benchmarks publishers across six drivers of subscription performance, suggests it is no longer the primary factor separating top performers from the rest. A mid-sized regional publisher can outscore a Top 25 National Publisher when the broader strategy is stronger. The biggest differences are increasingly tied to how publishers manage value across the subscription experience itself.

Publishers running dynamic subscription models consistently outperform those relying on static approaches across key measures of subscription health. The advantage shows up most clearly in average revenue per user (ARPU), the SPI driver most directly tied to sustainable revenue growth and often one of the fastest areas to improve.

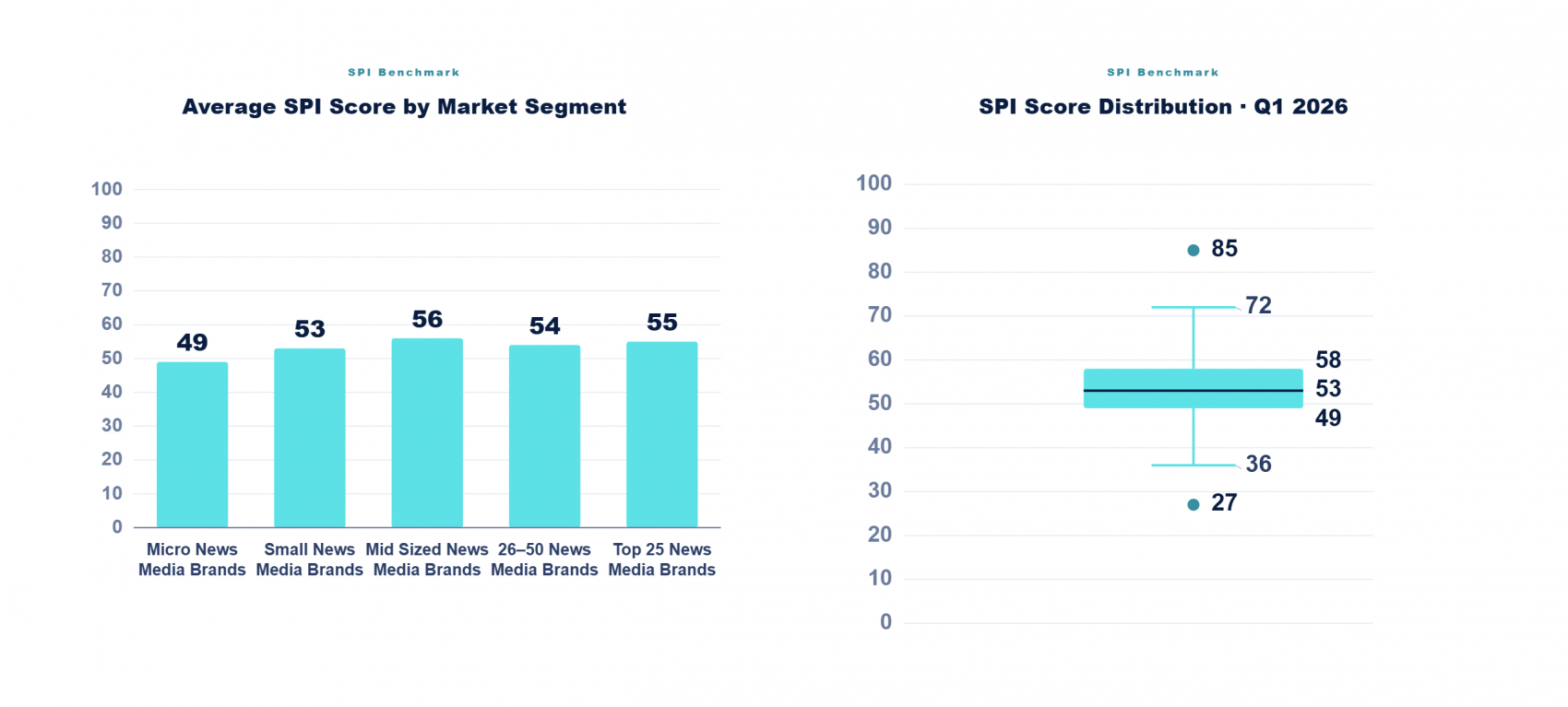

The SPI scores publishers from 0 to 100 across six drivers: audience growth, engagement, conversion efficiency, churn, ARPU, and subscriber penetration. Each driver is weighted by its impact on long-term revenue and benchmarked by market segment, recognizing that expectations vary by publisher size and region.

Based on Q1 2026 data, the analysis that follows examines where publishers stand on each of these drivers, what separates top-quartile performers from the rest, and how those differences translate into revenue.

Where the Industry Stands Right Now

At first glance, SPI performance appears clustered across market segments, with average scores ranging from the high 40s to mid-50s. But the publisher-level distribution tells a much more nuanced story. Individual scores range from 27 to 85, and performance does not always follow publisher size. Some micro brands outperform the Top 25 publishers, while some of the industry’s largest brands fall below the median score of 53. Scale can create advantages, but it does not automatically translate into stronger subscription performance.

Larger publishers do have real advantages, particularly the ability to drive audience growth through acquisition offers that smaller publishers often can’t sustain. But subscriber volume alone doesn’t create a strong subscription business. The real challenge is what happens after someone subscribes, and that’s where pricing, paywall, and engagement strategy tend to make the biggest difference.

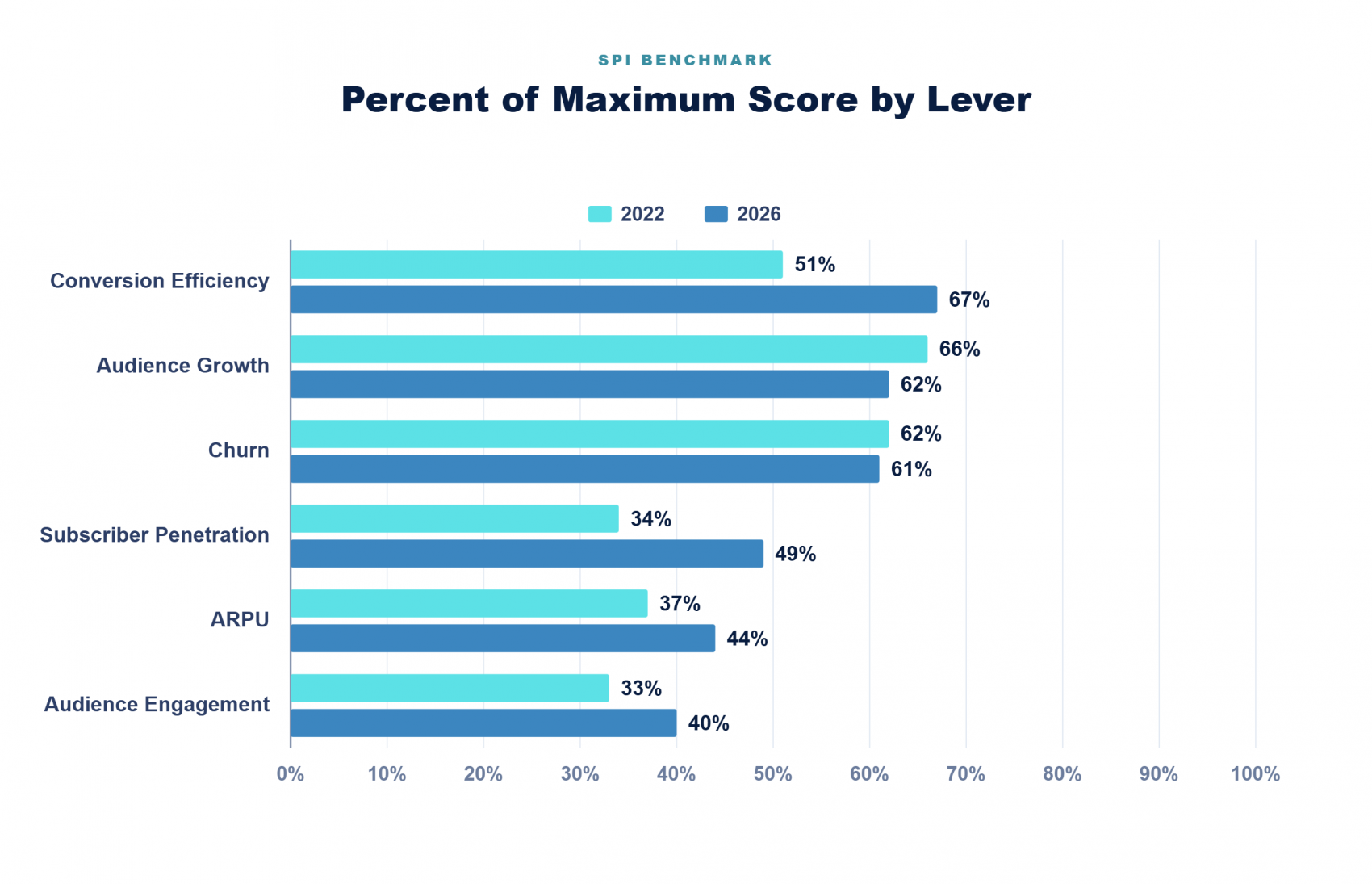

Looking at the six SPI drivers, the scores largely reflect where publishers have paid attention over the last decade. Audience growth remains one of the strongest-performing areas in the index. The strongest lever is conversion efficiency at 67% of the maximum score.

Looking at the six SPI drivers, the scores largely reflect where publishers have paid attention over the last decade. Audience growth remains one of the strongest-performing areas in the index. The strongest lever is conversion efficiency at 67% of the maximum score.

Subscriber-only content strategies helped publishers convert their existing readers more effectively, and that momentum has continued with the shift from static or segment-based metered models to dynamic paywalls that use real-time audience behavior and content signals to inform access and subscription decisions.

That progress is important, but converting readers is only part of the job. Publishers also need to keep subscribers engaged, retain them, and grow what they pay over time. That’s where opportunities stand today. Engagement remains the weakest driver in the index. It’s the part of the subscription model that bridges conversion and retention, and weaknesses there tend to show up later in churn and lifetime value.

At some point, subscriber growth must translate into revenue growth. That’s where ARPU stands out. At 44% of its maximum score, it’s one of the lowest-performing drivers in the SPI and one of the clearest signs that pricing hasn’t evolved as quickly as other parts of the subscription business. Many publishers still charge subscribers roughly the same price regardless of engagement or tenure, while publishers adopting more dynamic pricing approaches are increasingly separating themselves from the pack.

Many publishers still categorize subscribers into fixed pricing tiers, regardless of how engaged they are or how long they’ve been subscribed. This approach can be problematic because it means missing out on revenue from the most engaged and long-term readers who might be willing to pay more. Additionally, it can increase churn rates among subscribers who are already uncertain about their commitment. In recent years, dynamic pricing has gained popularity, and publishers who have embraced this model are noticing significant improvements in their ARPU scores.

The top quartile of the index averages $16.81 per subscriber per month, while the bottom quartile averages $11.05. For a publisher with 50,000 subscribers, that’s roughly $3 million in annual revenue, sitting in the difference between those two numbers.

The publishers with the strongest ARPU scores are not necessarily charging more. Rather, their performance reflects a strategy where pricing is more closely aligned with subscriber behavior, tenure, and perceived value. For many publishers, that makes ARPU one of the highest-return opportunities in the subscription business today.

Audience growth still matters, and engagement remains critical, but pricing is one of the few levers that can generate meaningful revenue gains without first acquiring additional subscribers.

What Top Publishers Are Doing Differently

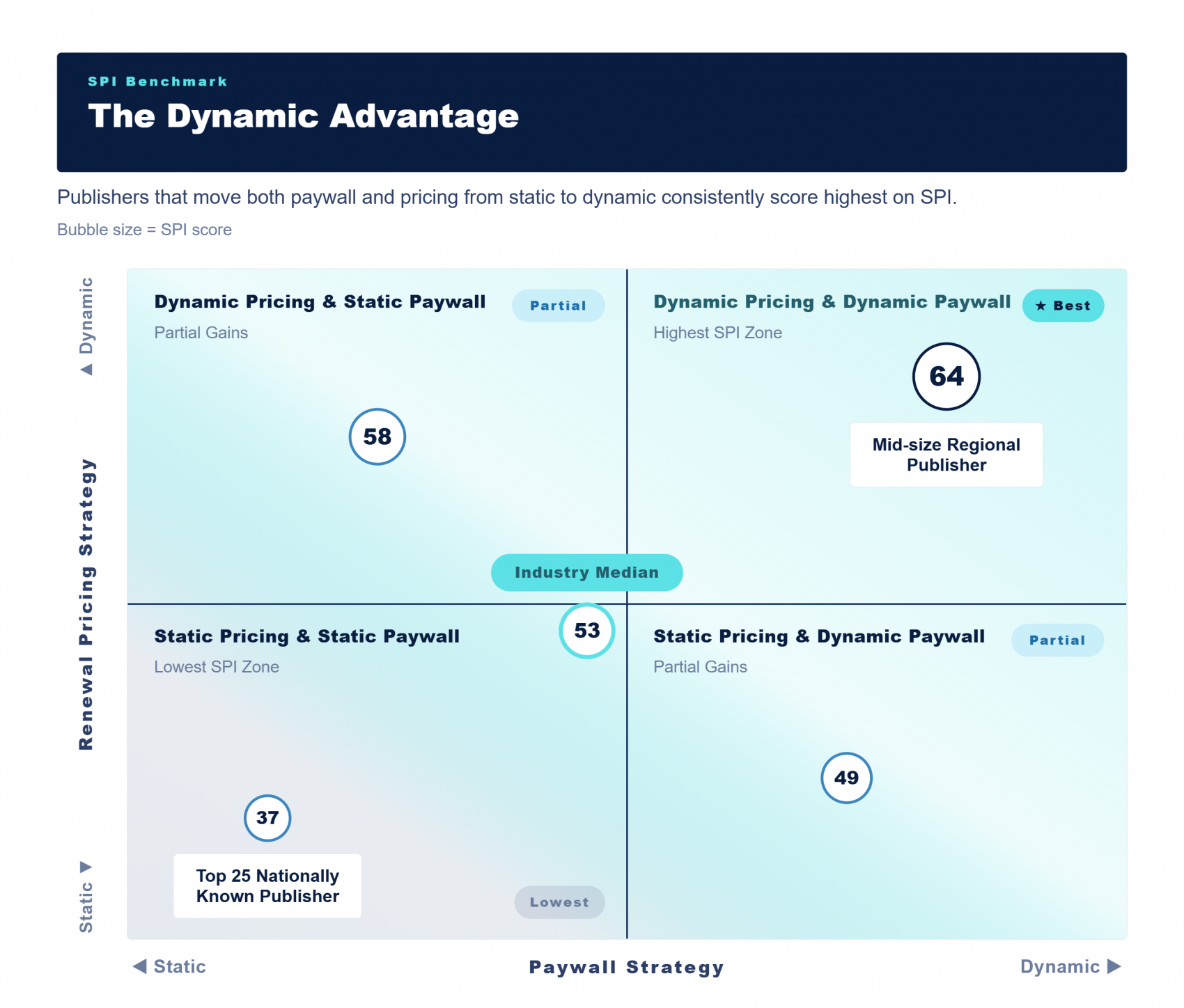

Publishers near the top of the SPI distribution don’t just outperform in one metric – they typically outperform across the lifecycle. What sets high-scoring publishers apart, more than anything else, is how far they’ve come in moving away from static paywall and pricing models toward something more intelligent and dynamic.

Publishers running static approaches on both consistently score at the bottom of the index. Those using dynamic paywalls informed by behavior like visit frequency, content type, and referral source, as well as ongoing dynamic pricing, score at the top. The ones in between who are invested in one but not the other typically land in the middle.

One mid-sized regional publisher committed to both: a dynamic paywall paired with targeted renewal pricing and offer testing. The result was that conversion efficiency improved 47% within a couple of quarters. Their total subscription volume rose 21% and their overall SPI score is in the top quartile.

The opposite example is a nationally-known publisher with one of the largest audiences within the benchmarking dataset and an SPI score that remains below the industry median each quarter. Their digital subscription model uses both a static paywall and flat pricing – where each subscriber is treated largely the same no matter their behavior. The publisher grew subscriber count significantly in late 2023, but ARPU fell and never recovered. A big audience and a static approach to monetization will only take you so far.

Publishers who have both, paywalls and pricing, tend to improve faster across multiple drivers — not just conversion or ARPU, but engagement and retention too. The ones who’ve stayed static on both are losing ground.

The Revenue Impact

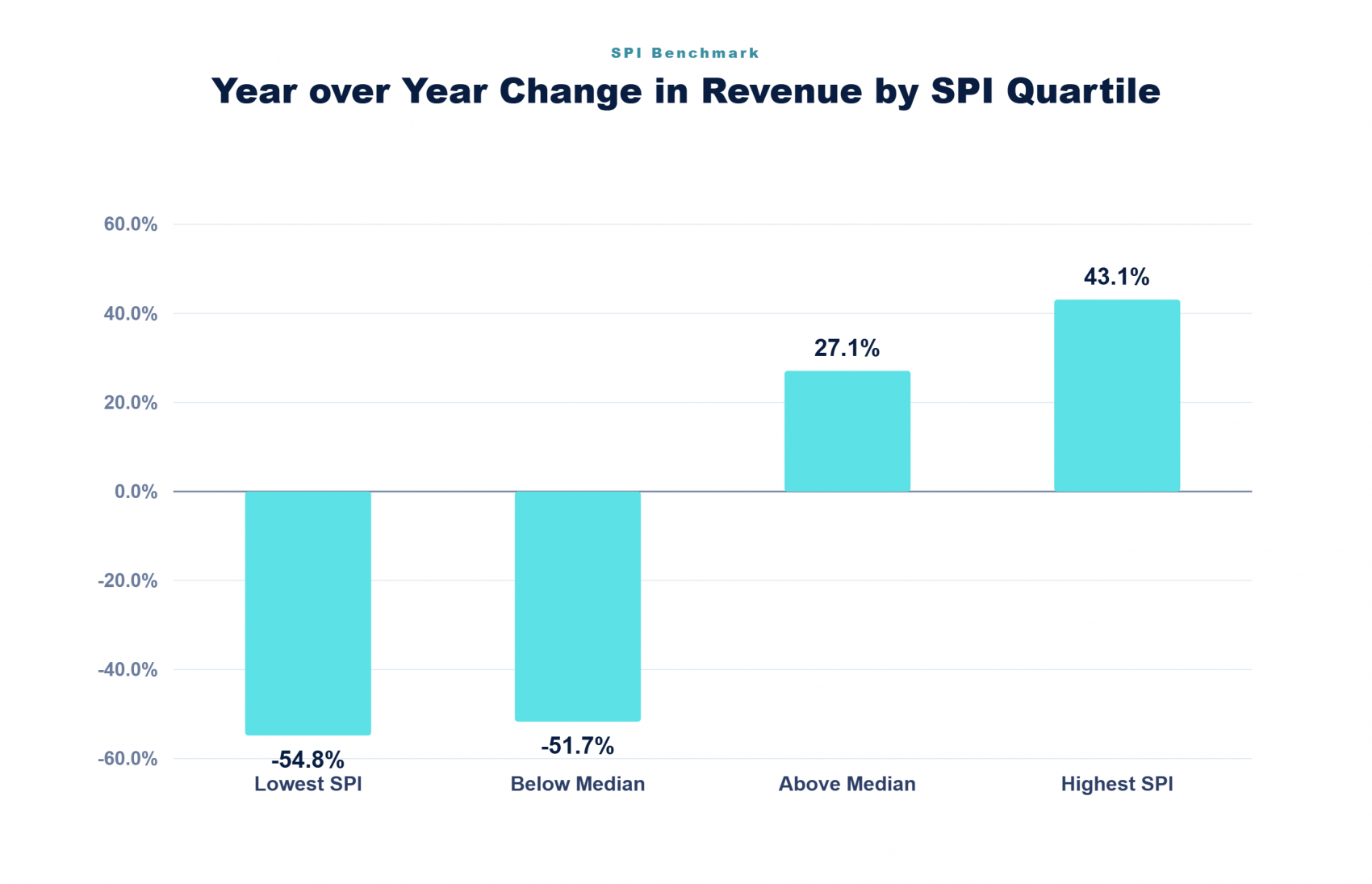

Higher SPI scores correlate with stronger revenue performance. Top-quartile publishers are growing revenue by 43% year over year. Bottom-quartile publishers are shrinking by roughly 55%.

Pricing is one of the fastest and most impactful levers. Most publishers who make deliberate and dynamic pricing changes start seeing movement within a quarter or two. One publisher increased its ARPU by 18% in a single quarter after implementing a targeted approach to pricing for digital subscribers. Their topline revenue was up 16% over the next three quarters.

Not every publisher sees gains at the same scale, but the relationship between SPI improvement and revenue growth is consistent. Publishers that improve their SPI scores tend to see real business growth alongside it.

The Path to Stronger Subscription Performance

Four years of SPI data point to the same conclusion: publishers that have taken a deliberate, dynamic approach to subscription growth are pulling ahead of those that haven’t.

Growing readers into subscribers, keeping those subscribers engaged, and ensuring pricing reflects what they actually value are three distinct jobs that must work together. The publishers seeing the strongest results are increasingly using dynamic approaches to all three — adapting paywalls, pricing, and engagement strategies based on reader behavior rather than treating every subscriber the same.

The encouraging part is that these gaps aren’t permanent. Publishers that adopt more dynamic models tend to improve their SPI scores over time, and those improvements translate into real business results. For many, pricing is the fastest place to start. Revenue impacts often appear within one to two quarters, making ARPU one of the quickest paths to measurable growth.

Not sure which growth lever deserves your team’s attention first? Connect with us to learn more about SPI and see how your subscription performance compares to industry peers.