Updated: January 19, 2022

Mather Economics will release its fourth quarter 2021 Benchmarking Reports by the end of the month.

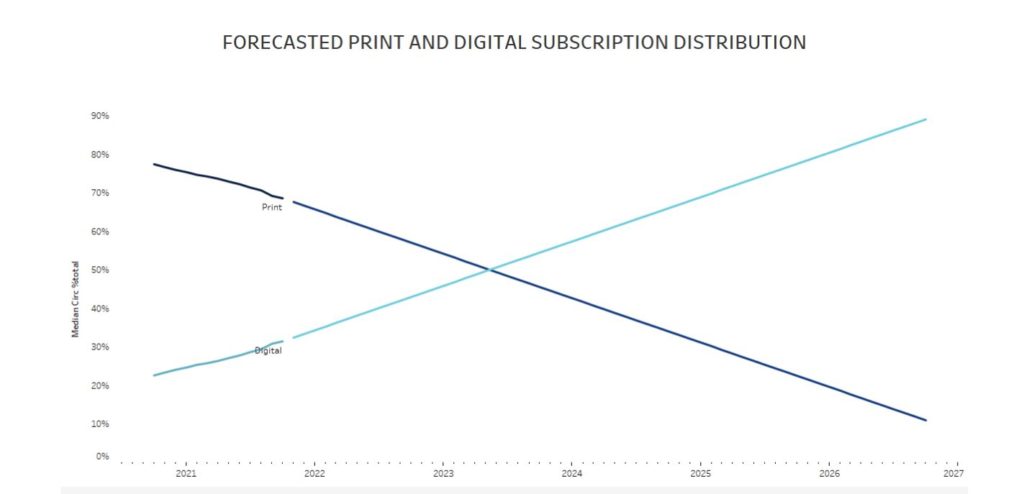

These Benchmarking Reports contain over a year’s worth of subscriber data, reported weekly, for digital only and hybrid (print + digital) subscribers from over 300 newspapers. In the Q3 2021 Report, Mather predicts how print ad digital subscription will be distributed until 2027. Our findings suggest:

- Digital only subscriber should exceed their print (including all-access) counterparts at some point between 2023 and 2025.

- Raising rates on digital only subscribers will be critical to maintaining a robust revenue base.

For more information on how to receive these reports, connect with the pricing experts at info@mathereconomics.com.

Let us help you on your print to digital subscription journey.

This metric includes new digital subscriptions from all sales channels, not just the metered paywall. The median value of this metric is 388 digital starts per month for every 1 million unique visitors.

Top performing publishers average over 600 starts per million visitors, and we work with a few publishers that have over 1,000 starts per million visitors per month. These publishers are actively analyzing which content is most effective at converting users to digital subscribers, and they produce more of that content and market it effectively.

Don’t hesitate to connect with Matt Lindsay and the experts at Mather Economics to help you on your print to digital subscription journey.